The New York Times reported on June 23 that Mark Zuckerberg directed a small team to build a prediction market app, internally called Arena, where users would forecast outcomes in politics, sports, and world affairs using points.

The company that renamed itself for a virtual world that has produced nearly $90 billion in cumulative Reality Labs operating losses is now chasing prediction markets, a category with real demand, a proven user base, and enough regulatory complexity to make this either the smartest pivot Meta has attempted or the most familiar kind of expensive mistake.

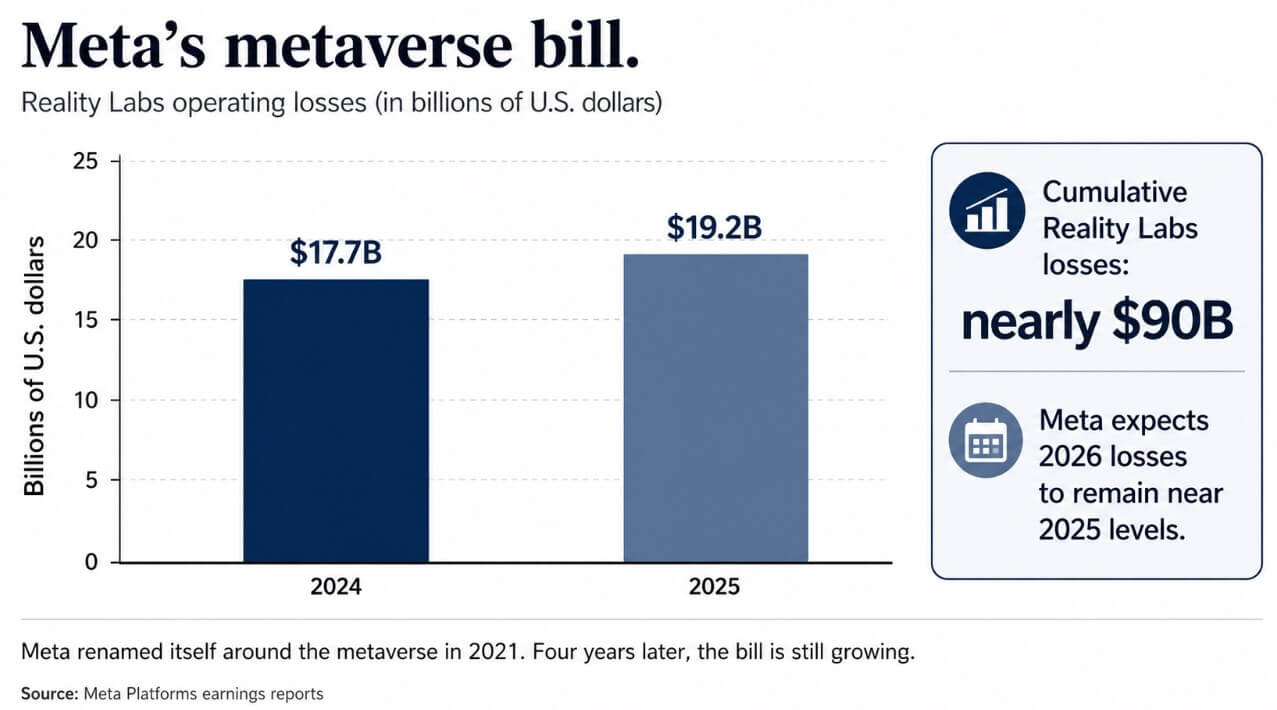

The metaverse bill

When Meta changed its name from Facebook in October 2021, Zuckerberg wrote that the company’s focus would be to bring “the metaverse to life,” predicting it would reach a billion people within a decade.

Reality Labs, the division tasked with delivering that vision, reported operating losses of $17.7 billion in 2024 and $19.2 billion in 2025, bringing cumulative losses to nearly $90 billion. Meta told investors it expects 2026 losses to land near 2025 levels.

Horizon Worlds, the flagship social VR platform, was reported in 2022 to have fallen below 200,000 monthly active users after Meta had targeted 500,000 and later revised that goal lower. Meta later moved to phase out the VR version in 2026.

Why prediction markets are a different category

Kalshi and Polymarket have already pushed combined monthly trading volume to roughly $24 billion in 2026, with current projections putting annual prediction-market volume above $130 billion.

Robinhood launched a prediction markets hub in 2025, Interactive Brokers integrated event contracts into its platform, and prediction markets appeared in the Golden Globes telecast.

In this landscape, Bernstein estimated in April that the sector could reach $1 trillion in annual volume by 2030.

Meta also has a documented record of copying hot formats and winning through distribution, with examples such as Stories arriving on Instagram once Snapchat had built the format, Threads launching into a market Twitter had owned for a decade, and Reels arriving well into TikTok’s dominance.

All of these products found audiences because Meta had 3.56 billion daily active users across its apps as of April, a scale that dwarfs that of any prediction market platform.

Arena’s points-first design follows the same playbook of absorbing a behavior users already want, embedding it in the attention machine, and letting reach do the work originality once did.

A prediction market app requires software, feeds, identity, moderation, compliance infrastructure, and possibly a regulated partner.

The metaverse required custom hardware, immersive content, avatar systems, operating environments, and years of behavioral adaptation. The losses at Reality Labs show how expensive the manufactured future model becomes.

| Category | Metaverse push | Arena / prediction markets |

|---|---|---|

| User demand | Meta tried to create a new social behavior | Users already trade, forecast, and argue over outcomes |

| Product requirement | VR headsets, avatars, immersive worlds, operating systems | App, feed, identity, points, moderation, compliance |

| Distribution model | Requires users to enter a new virtual environment | Can plug into Facebook, Instagram, WhatsApp, and Meta AI |

| Market proof | Horizon Worlds struggled with retention and scale | Kalshi, Polymarket, Robinhood, and Interactive Brokers already show demand |

| Cost structure | Hardware-heavy and capital intensive | Mostly software and compliance infrastructure |

| Core risk | Users never fully migrated | Users arrive, but regulators and journalists do too |

Arena is Meta’s second attempt

In 2020, Meta launched Forecast, a points-based crowdsourced prediction app focused on current events during the early COVID period.

Meta shut it down in 2022, before Polymarket’s breakout during the 2024 presidential election, Kalshi’s legal victory over the CFTC on election contracts, and the sector crossing $50 billion in annual volume.

The sector Meta is entering has an enforcement history: the CFTC ordered Polymarket to pay a $1.4 million penalty in 2022 for operating an off-exchange event-contract platform as an unregistered derivatives venue.

Kalshi fought a multi-year federal court battle to offer election contracts, winning at the district level in September 2024.

The CFTC dropped its appeal in May 2025, opening the door to election event contracts while keeping political and integrity objections on the agenda.

In April 2026, the CFTC filed its first-ever insider trading complaint tied to prediction market activity, alleging an active-duty US Army officer traded Polymarket contracts using classified intelligence about a Venezuela operation.

Meta’s own history with financial infrastructure makes regulators alert to its ambitions here.

The Diem Association, the Facebook-backed digital currency project, sold its assets to Silvergate in 2022 when policymakers concluded that giving Meta control over a payment network used by billions of people created unacceptable concentrations of financial and social power.

Meta’s combination of social identity, political content, financial incentives, and market data generated the most hostile reception during the Libra hearings.

A points-based forecasting game deflects those regulatory risks at launch, which is why Meta is starting there.

What distribution buys

The most plausible first version of Arena is a social forecasting layer built on distribution and social scale: Instagram creators posting markets on award shows, Facebook Groups arguing over sports odds, WhatsApp communities circulating crowd consensus, and Meta AI summarizing what the network believes will happen.

This version would sit below the real-money event-contract layer that brought enforcement action against Polymarket and years of litigation around Kalshi, while running through a social graph of 3.56 billion daily users.

Prediction markets depend on financial stakes to discipline forecasting and produce accurate prices. Swap financial stakes for engagement incentives, and the product tilts toward virality and time-on-platform over accuracy.

Meta’s long record on political content and misinformation gives regulators and journalists a pre-built frame for every controversy Arena generates.

The bull case is that Meta’s distribution advantage proves large enough to build real category scale. Stories and Reels succeeded by taking behaviors users already liked and pushing them through platforms with billions of daily users.

If Arena builds a social forecasting layer that keeps financial stakes manageable and makes prediction markets accessible to a mass audience that uses Facebook and treats Kalshi as a specialist product, Meta could expand the category in ways that benefit the established platforms too.

Crypto-native and financially literate users turned prediction markets into a category now projected to process more than $130 billion in annual volume. Meta’s 3.56 billion daily active people are the mass audience the sector has never touched at scale, and that demographic distance is the opportunity.

The bear case is that the combination of political markets, creator incentives, engagement optimization, and Meta’s institutional record makes Arena a regulatory and reputational target before it reaches scale.

Regulatory scrutiny of insider trading in prediction markets was already intensifying when Meta’s reported entry surfaced, with the CFTC’s first-ever event-contract insider-trading complaint filed just two months earlier.

A Meta-owned prediction market covering elections, sports outcomes, and political figures gives regulators a recognizable reason to move, and Meta’s track record on politically sensitive content means the company enters this space with a credibility gap its scale has historically deepened.

| Scenario | What Arena looks like | Why it works or fails | Impact on prediction markets |

|---|---|---|---|

| Bull case: Meta makes forecasting mainstream | Points-based social app with creators, leaderboards, sports, entertainment, and Meta AI summaries | Distribution turns prediction markets into a mass consumer habit without triggering immediate betting scrutiny | Expands the category and sends more serious users toward Kalshi, Polymarket, Robinhood, and IBKR |

| Base case: viral but shallow | Arena becomes a social game, not a serious market | Points create engagement but weak forecasting discipline | Helps awareness but does not threaten real-money platforms |

| Bear case: Facebook makes it toxic | Political markets, creator spam, misinformation, and engagement bait dominate | Meta’s reputation turns every bad market into a regulatory story | Regulators scrutinize the whole sector more aggressively |

| Black swan: real money arrives too soon | Meta partners with or builds toward regulated event contracts | Politics, sports, and money collide before trust is earned | Triggers backlash similar to Libra/Diem and could pressure crypto-native markets |

The company’s financial products have collapsed before when policymakers decided the trust question was settled.

Arena could succeed because prediction markets already exist and already have users. The platform building it carries the same reputation it had when Libra collapsed in a category where trust, once elections and money enter the picture, is the one asset that scale has to earn before it can spend.

Analysis,Featured,Market,Metaverse#Meta #prediction #markets1782334058