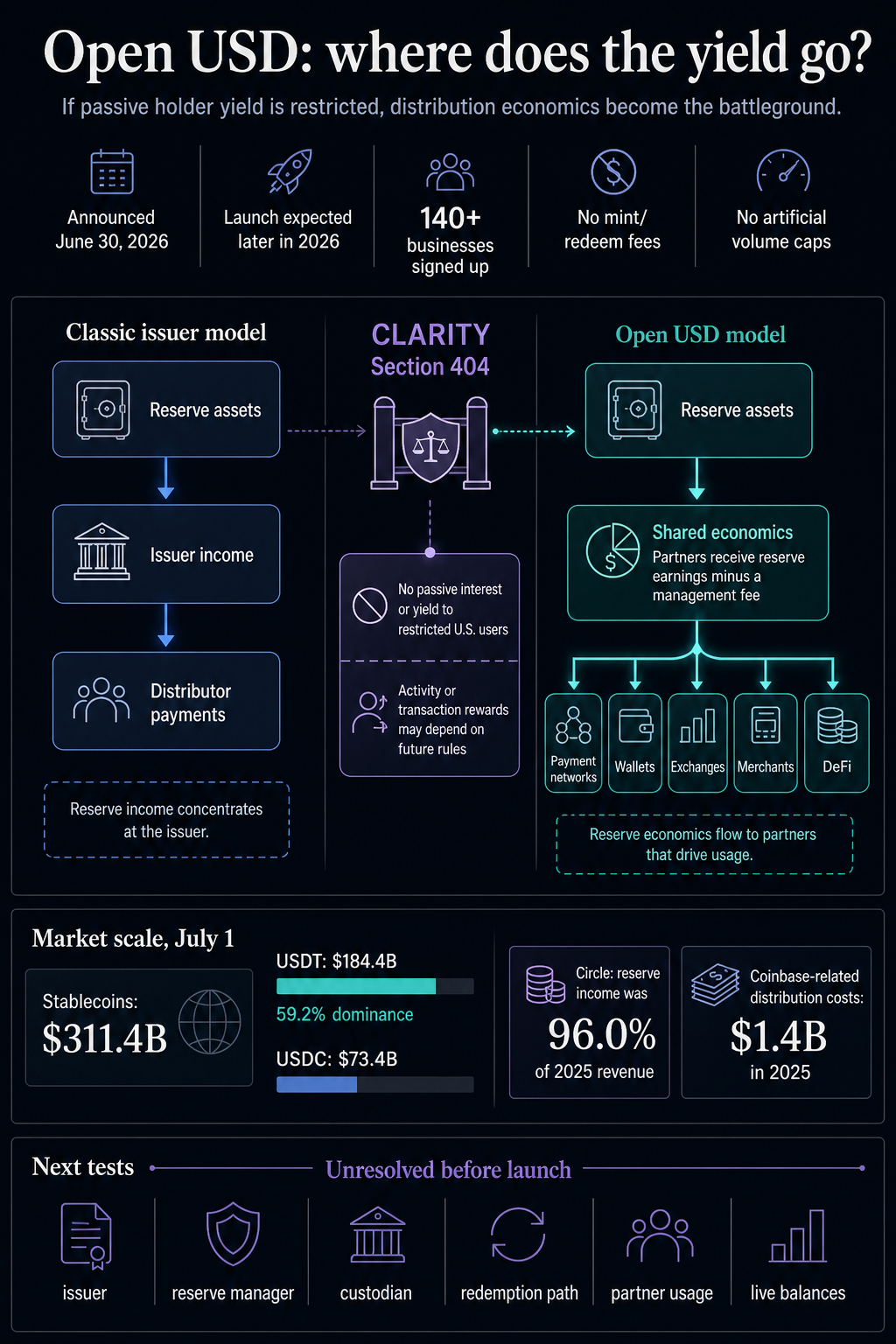

Open Standard’s Open USD is trying to make the stablecoin yield fight about distribution before the token is live.

The company announced Open USD on June 30 as a stablecoin for global money movement. Its headline feature is a reserve-sharing model: businesses can mint and redeem at no cost, without artificial volume caps, while partners receive reserve earnings minus a small management fee.

Open Standard also says Open USD will be operated by an independent company with partner-led governance. Founding CEO Zach Abrams framed the product as a stablecoin built by and for the businesses that will use it.

Open USD has yet to show live supply, redemption history, reserve attestations, or a visible place in stablecoin market tables. It is expected to launch later in 2026.

Even so, its stated design points directly at the most contested part of the stablecoin business: reserve economics.

If U.S. rules limit passive yield to stablecoin holders, Open USD‘s bet is that the fight moves elsewhere. Instead of paying users to sit on tokens, the economic value can flow to merchants, payment processors, wallets, exchanges, marketplaces, DeFi venues, and other companies that drive transaction volume.

Open USD puts distribution at the center

Open Standard’s pitch is simple in public but aggressive in market structure. It describes Open USD as shared infrastructure and says participants can earn revenue based on usage.

Its announcement lists more than 140 businesses across payments, finance, technology, commerce, and crypto, including Visa, Stripe, Mastercard, BlackRock, BNY, Google, Coinbase, Solana, Base, Aave, Ripple, Fireblocks, Shopify, and DoorDash.

The partner list maps where the economics could flow. Payment networks control merchant access. Exchanges and wallets control where balances sit. Marketplaces control payout flows.

DeFi protocols control liquidity venues, while banks and asset managers control the plumbing for trust, custody, and reserves. If those firms can share in reserve economics, a stablecoin issuer’s traditional advantage becomes a distribution negotiation.

That is why Open USD reads as an attempt to turn stablecoin float into partner compensation. In the classic model, reserve income is the issuer’s economic engine.

In Open Standard’s stated model, most of that value is supposed to return to the companies that adopt and distribute the stablecoin.

The caveat is large. Open Standard’s public materials say reserves are maintained at major financial institutions in compliance with U.S. regulatory requirements, but they have yet to fully identify the legal issuer, reserve manager, custodian, redemption counterparties, or reserve composition.

Those details determine whether the model can satisfy both compliance and marketing teams.

The strongest economic comparison is Circle. Circle’s 2025 Form 10-K says reserve income represented 96.0% of 2025 revenue and that reserve income depends on stablecoins in circulation and the reserve return rate.

The filing also shows that distribution is already expensive. Circle reported $1.4 billion of Coinbase-related distribution costs in 2025 and described allocations to Coinbase tied to USDC held on Coinbase’s platform and broader ecosystem growth.

Coinbase’s 2024 Form 10-K tells the other side of the same arrangement. Coinbase says its stablecoin revenue from Circle is determined by daily income generated from USDC reserves.

That revenue has exposure to USDC market capitalization, platform balances, approved ecosystem participants, deducted expenses, and interest rates.

Those filings make Open USD’s market signal sharper. Reserve economics are already moving between issuer and distributor in USDC’s ecosystem.

Open USD proposes to make that bargain more explicit and more widely available to the companies that can drive usage.

Tether sits in a different category. DeFiLlama stablecoin data showed a total stablecoin market capitalization of near $311.4 billion on July 1, with USDT at around $184.4 billion and 59.2% dominance, while USDC was at around $73.4 billion.

CryptoSlate’s market pages showed a similar gap, with USDT having a far higher 24-hour trading volume than USDC, at $67 billion in exchange volume and $1.5 billion in DEX volume. USDC recorded a sizeable yet smaller $10.8 billion in exchange volume and $1.9 billion in DEX volume.

Tether’s moat extends beyond reserve yield. It is offshore dollar liquidity, exchange integration, settlement habit, and deep trading-pair usage.

Open USD can pressure that over time only if it becomes liquid across venues and geographies. Its earlier challenge is to Circle’s institutional claim that USDC is the default regulated stablecoin rail for businesses that need compliance, transparency, and distribution.

CLARITY turns yield into a routing problem

The policy backdrop gives Open USD its opportunity.

Section 404 of the Senate Banking Committee’s Digital Asset Market Clarity Act draft would prohibit covered parties from paying direct or indirect interest or yield tied to payment stablecoin balances to restricted U.S. customers or users.

The same section preserves room for bona fide activity-based or transaction-based rewards under future rules.

That distinction is where Open USD fits the current debate. If law and regulators draw a hard line around passive, deposit-like yields to holders, the market still has to decide whether businesses can be rewarded for actual distribution, transactional activity, or commercial use.

Open USD’s shared-economics model sits in that zone.

Open USD functions as a policy stress test. Its public materials describe partner economics and distribution incentives, while the final treatment of merchant rewards, exchange incentives, wallet rebates, and partner revenue shares depends on law, rulemaking, and program design.

The White House Council of Economic Advisers has argued that a prohibition on yield-bearing stablecoins would do little to protect bank lending while sacrificing consumer benefits.

The Bank Policy Institute has argued the opposite: that yield-bearing stablecoins can reduce deposits and lending after households and businesses adjust their balance sheets.

Open USD leaves that fight open. It changes the underlying business question.

If the law makes passive user yield harder, the next fight may be over whether reserve economics can be paid to the companies that enable stablecoin transactions.

That creates the tension Open USD is built around. A holder reward looks like a consumer finance product; a partner revenue share looks like a commercial distribution arrangement.

The final rules will determine how much distance must exist between those categories, which parties can receive economic benefits, and what disclosures or controls companies need before reserve value can flow back to platforms that originate usage, rather than directly to end users.

That makes rule-writing important for each link in the distribution chain. A payment network, wallet, exchange, or marketplace can all help generate usage, but their incentives may be reviewed differently depending on who receives the payment and whether it reaches restricted U.S. users.

Usage is the next test

Open Standard’s partner list is unusually strong; reported balances remain the adoption test.

The launch test is practical. The market needs to see who issues Open USD, where the reserves sit, what backs them, how redemptions work, which chains launch first, which partners actually route money through it, and whether balances appear in market data after launch.

Until then, Open USD remains a serious proposal with credible distribution names and the incumbent test still ahead.

The implication is practical. Open USD can pressure Circle by turning USDC’s existing reserve-income bargaining problem into a product feature.

It can pressure stablecoin regulation by showing that yield debates extend beyond the holder’s wallet. It can pressure payment and merchant platforms by giving them a reason to treat the choice of stablecoin as an economic decision, alongside infrastructure and compliance.

The model still has to prove that the partner board, reserve structure, compliance model, redemption path, and actual usage can survive launch.

If that evidence never appears, the announcement remains a warning shot. If it does, the stablecoin war shifts from a fight over which issuer keeps the float to a fight over which network can share it without breaking the rules.

Banking,Featured,Lending,Opinion,Regulation,Stablecoins,USDC,USDG,USDT,xrpUSDC,USDG,USDT,xrp#OpenUSD #answer #bank #push #CLARITY #Hints #stablecoin #yield #concessions #fail1782934312